Updated on 13 May 2026

At a glance: The provisional budget of a customer project in IT Services or consulting firm sets the margin at completion in advance. This article reviews its 8 components, the 7-step method to build it, the 6 pitfalls to avoid in a service company, and the mechanism that goes from the provisional budget to the real-time forecast margin.

In a IT Services or a consulting firm, the provisional budget of a project is valid for the 6 to 18 months following the estimate. It sets out what the project costs, what it brings in, and the margin that the company can keep at the close. Three lines of the income statement depend on the quality of this budget: the recognized turnover, the gross margin per practice, and the occupancy rate of consultants.

In practice, the cause of a crumbling project margin is almost never the unexpected. It is a provisional budget built on assumptions that are not verified at the time of the quote: undervalued subcontracting, ADR poorly calibrated, unverified package-control mix, or absence of hazard.

This article reviews the components of a projected project budget in a service company (fixed-price, direct, mixed), a 7-step method to build it before the kick-off, the most common pitfalls in IT Services and consulting firm, and the mechanism for switching from the provisional budget to real-time forecast margin monitoring.

🔎 What to remember about the provisional project budget in IT Services or consulting firm

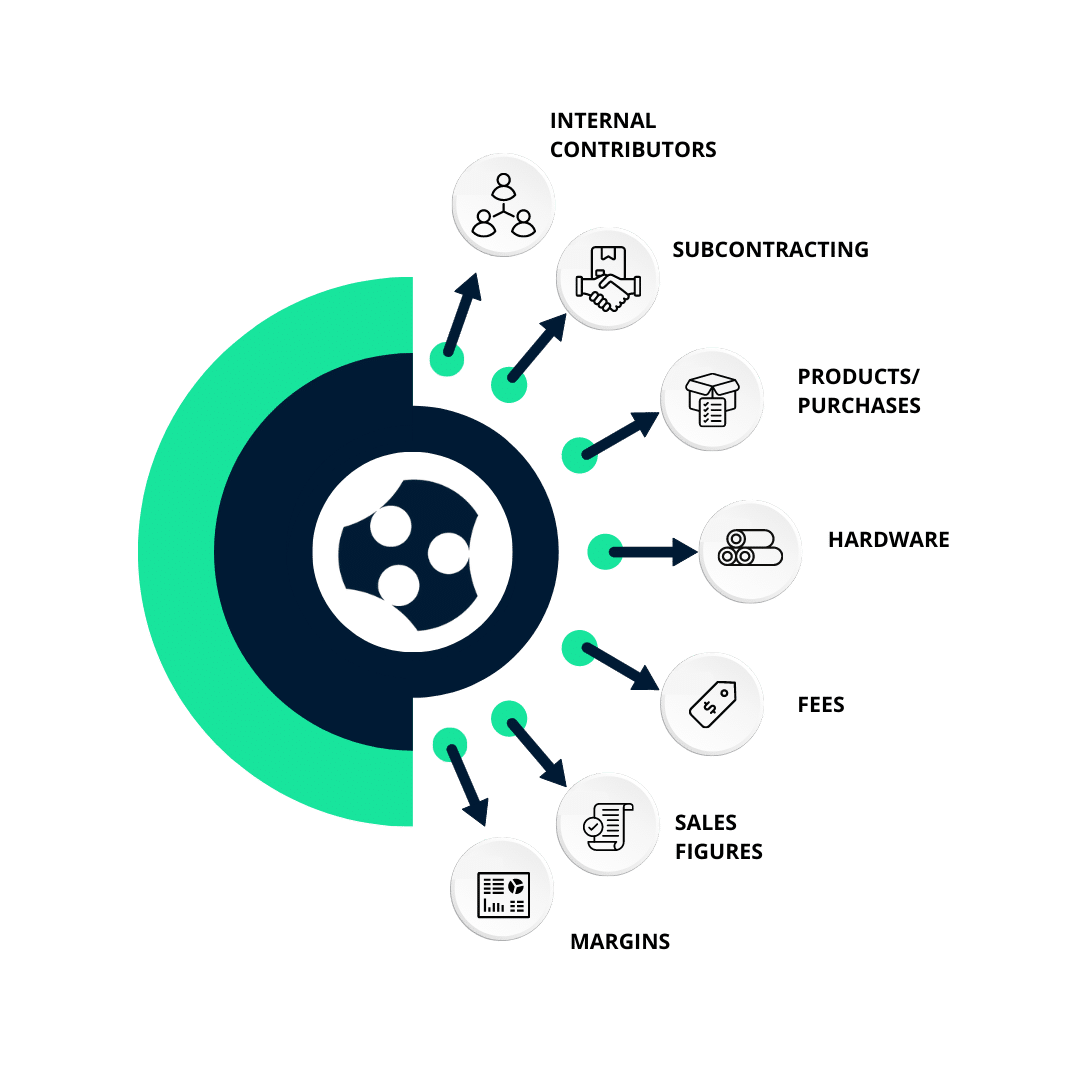

- A provisional project budget for a service company covers 8 lines : internal contributors, subcontractors, products, equipment, rebillable costs, turnover (fixed/direct/mixed), target margin, contingency.

- The method goes through 7 steps, from the framing of the scope to the construction of the project income statement, all of which are laid out before the kick-off.

- Three pitfalls explain most of the abuses in service companies : ADR poorly calibrated, subcontracting not costed, no hazard.

- The provisional budget only has operational value when compared to the real-time forecast margin : which Excel does not calculate.

What is a provisional project budget?

The project budget is the most important financial management tool for a service company mission. Its operational definition, its distinction from other company budgets, and its difference from the customer quote need to be clarified before addressing its components.

Definition and difference between budget / provisional budget / actual budget

The provisional budget of a project is the estimate, made before the kick-off, of all the costs and turnover that the project will generate during its duration. It takes into account direct costs (contributors' man-days, subcontracting, fees) and indirect costs (equipment, licenses, re-invoiced overheads). On output, it gives a target margin that the company undertakes to keep.

Three concepts are often confused:

- Budget. Numerical target for a period of activity (month, quarter, year). Its granularity is the company or the practice, not the project.

- Provisional budget. Estimate projected before implementation. On a project, it is placed once before the kick-off and serves as a reference for the entire duration of the project.

- Actual budget. Observation of what has actually been spent and invoiced. It is calculated at the end of each period and is compared to the provisional budget to measure the variance.

The margin at completion combines the two: it compares the initial provisional budget with the cost consumed to date plus the cost of the remaining costs.

The 3 types of project budget

On a project in a service company, three types of budget coexist and are used for different trade-offs.

- Provisional budget. The estimate made before the kick-off, which sets the target margin. It is rarely revised. It is used at the time of customer signature and during amendment arbitrations.

- Budget committed. The part of the provisional budget that has been contracted: subcontracting orders signed, man-days planned on the project sheet, product purchases validated. It is used to anticipate cash and to avoid overruns before they are consumed.

- Budget achieved. The cost and turnover actually recorded to date. It is calculated at the end of the period and feeds into the company's financial reporting.

For some long projects, a fourth budget exists: the landed budget, which projects the final result by combining what has been achieved and what remains to be done. This is the purpose of the budget landing.

Provisional budget vs. quote vs. specifications vs. business plan

The provisional budget is often confused with three other documents that are nevertheless distinct.

- Quote. Commercial document that costs the project from the customer's point of view. It shows the sale price, the payment terms, the scope delivered. The provisional budget quantifies the project from the point of view of the service company: it also includes the internal cost, the target margin and the contingency, data that are absent from the customer quote.

- Specifications. A functional document that describes what the project is to deliver. It is the input of the provisional budget, not its equivalent.

- Business plan. Prospective financial view of a global activity or practice over several years. The projected project budget is a brick of the business plan, not its summary.

A project sold for €100k to the client can have a provisional budget with €70k of internal cost, €18k of target margin and €12k of contingency. These three figures do not appear in the estimate.

Why make a provisional budget in IT Services or consulting firm?

Without a provisional budget, a service company pilots on a month-to-month basis. With a project-by-project structured provisional budget, it has a consolidable margin target by practice, by key account and by financial year. This difference changes the nature of commercial management and cash flow: resource allocation decisions are made on figures, not on impressions.

Six objectives structure a provisional project budget for a service company

- Allocate resources. Distribute man-days between internal profiles and subcontracting, in line with the overall workload plan.

- Quantify the return on investment. Calculate the target margin and compare it with the gross margin objectives per practice. A low-margin project can be accepted if strategic, but this decision is conscious.

- Control and control while running. The budget becomes the project manager's roadmap and the reference for the weekly project committee meetings.

- Empower stakeholders. The budget sets the objectives of each contributor on his or her tasks and makes the origin of an overrun transparent.

- Facilitate the decision on an amendment. When the customer requests a change of scope, the decision is made with a clear costing, not an estimate on the spot.

- Secure the margin from the quote. By setting the internal cost, the hazard and the target margin before signing, the company avoids accepting a project with an unidentified negative margin.

Download our project budget table template

Track your KPIs and check the reliability of your projects.

The specificities of the customer project in IT Services or consulting firm

Five specificities distinguish the provisional project budget in a service company from a generalist project budget.

- The main cost is human. Consultants' man-days often account for 70 to 85% of the total cost. The calculation of the ADR per profile becomes the critical data, more than the material cost.

- The contractual mode varies. The same project can be sold on a fixed-price basis, on a time-based basis, or in mixed mode. Each mode changes the way in which revenue and target margin are quantified.

- Subcontracting is integrated into the heart of the project. Many projects in IT Services use freelancers or other service providers with specialized skills. The costing of subcontracting is as structuring as that of internal contributors.

- Inter-contract weighs on the margin. A consultant who is not staffed between two projects remains paid. The provisional project budget feeds the arbitration resource planning practice.

- Fees are often rebillable. Travel, accommodation, catering: depending on the contract, these costs are re-invoiced on an actual or fixed basis. This distinction changes the project income statement.

When to establish, when to revise, who establishes

When to establish. The provisional project budget is built before the contract is signed, based on the estimate and the specifications. On a recurring project or a key account, it is reviewed at the beginning of each financial year by integrating known commitments.

When to revise. Three cases require revision (see below the section on rebudgeting): change of customer scope validated by amendment, margin drift without cause perimeter, or internal decision to reinvest. Apart from these cases, the initial budget remains the reference for preserving the readability of the follow-up.

Who establishes. On a service project, the construction of the provisional budget involves three roles:

- The project manager quantifies the scope, estimates man-days and identifies subcontracting needs;

- The practice or mission director validates the ADR, target margin levels and profile arbitrages;

- The project management controller or CFO checks the consistency with the company's budget assumptions and the projected workload plan.

On a strategic project, the sales department enters the loop to match the selling price to the margin objectives.

What are the components of a project budget?

A provisional project budget for a service company is built line by line. Missing a line or undervaluing it changes the project's commitment arbitration. Eight components structure the budget by IT Services and consulting firm. The separation between internal cost, external cost, costs and turnover gives readability to the project income statement.

Project resources

Internal contributors and their ADR by profile

Internal contributors are the consultants, engineers, project managers and support functions of the company who dedicate time to the project. To quantify their cost, two pieces of data are sufficient: the number of man-days per profile and the ADR of each profile.

Example of a production plan in Stafiz

The ADR cost is not the ADR charged to the customer. It includes the salary, bonuses, benefits, and the share of the indirect cost allocated (premises, tools, supervision). A practice that does not calculate its ADR costs correctly systematically underestimate the cost of its projects.

Depending on the contractual method, the unit of costing varies:

- On a fixed-price project, the unit is the day or half-day per task.

- On a time-based project, the unit is the day invoiced to the customer (which may differ from the day consumed internally).

- On a mixed project, the two units coexist and the budget explicitly separates them.

Subcontracting

Numerous projects in IT Services or consulting firms use subcontracting, either to meet a one-off need for skills, or to absorb a peak in load. Three lines appear in the budget:

- The purchase price from the subcontractor (ADR or lump sum depending on the contract);

- The resale margin applied to subcontracting (covers the cost of management and the financial margin);

- The payment window to the subcontractor vs. the customer collection window (impact on project cash flow).

Unencrypted subcontracting is one of the three main pitfalls identified in margin drifts (see the section on pitfalls below).

Products and purchases/licenses

Some projects involve the purchase of products made available to the customer: software licenses, hardware, equipment. The budget includes the purchase cost and the resale margin applied. The window between order and delivery influences the project schedule: a supplier delay can postpone the start of the tasks that depend on it.

The equipment and its depreciation

When a project uses the company's own hardware (servers, test equipment, tooling), the depreciation cost over the life of the project is included in the budget, not the initial purchase cost. When equipment is rented for the needs of the project, the rent over the duration of use enters the budget.

Rebillable vs. non-rebillable expenses

The costs incurred on a project in a service company are divided into two blocks:

- Rebillable fees. Travel, accommodation, catering, parking. Depending on the contract, they are re-invoiced on an actual basis (exact amount of receipts) or on a fixed rate (fixed amount per day or per mission). They appear in cost and turnover in the budget.

- Costs that cannot be rebilled. Costs that the company absorbs without re-invoicing: internal tools specific to the project, pre-sales fees, onboarding consultant onboarding fees. They only appear in cost.

The customer repayment window can weigh on the project cash flow: a fee advanced in January reimbursed in April freezes cash over 3 months.

Turnover: fixed price, control room or mixed mode

The contractual method of selling the project changes the way in which turnover is quantified.

- Fixed-price project. The total sale price is set at the time of signing, regardless of the time actually consumed. The turnover of the provisional budget is known from the estimate. The margin risk relates only to the cost: an excess of man-days does not translate into additional turnover.

- Project under direct management. The customer buys man-days at one ADR invoiced. The turnover varies according to the time actually consumed. The provisional budget projects an indicative number of days over the duration of the contract, which can be capped by the customer.

- Mixed-mode project. Part of the project is sold on a fixed-price basis (a specific deliverable), the other on a self-managed basis (additional man-days for evolutions). The budget explicitly separates the two blocks because they are not managed in the same way.

The contractual method also weighs on the target margin: on a package, the margin is entirely linked to compliance with the initial costing; on a public authority, it depends on the ADR billed minus ADR cost; On a mixed farm, the two logics coexist and the budget must distinguish them in order to remain arbitrable.

The target margin

The margin of a project is the difference between the projected turnover and the total estimated cost. There are three levels of margin:

- Project gross margin. Projected turnover minus projected direct cost (internal man-days valued at ADR cost, subcontracting, non-rebillable costs). This is the operational level followed by the project manager.

- Net project margin. Gross margin minus allocated overheads (management, support functions, sales cost). This is the level followed by the practice director.

- Margin to termination. Gross or net margin projected at closing, including what has been achieved to date and what remains to be done. This is the level followed by the CFO in consolidation.

Each practice sets its target margin levels by type of project. A strategic project can be accepted at a low gross margin if the commercial angle is consolidated.

Hazard and the provision of risks

The contingency is the provision of risks integrated into the provisional budget to absorb unforeseen events that are not attributable to a specific item. It does not appear in the customer quote: it is internal data of the company.

Three calculation practices coexist in a service company:

- Lump sum percentage. A fixed percentage of the total cost is provisioned (often between 5 and 15% depending on the project risk). This practice is simple but blind to the nature of the risks.

- Hazard by position. Each budget line has its own provision: 10% on subcontracting, 5% on internal man-days, 20% on specific purchases. The method requires that the risks be explained by position.

- Hazard based on the risks identified. The hazard is calculated from a list of individually quantified risks (probability × impact). This is the most rigorous method, recommended for projects with high technical uncertainty. See also how to perform a project management risk analysis.

A provisional budget without explicit contingency transfers the risk to the target margin: this is one of the three main pitfalls identified in a service company.

How to establish a project budget in 7 steps

Build a project budget in IT Services or consulting firm follows a seven-step sequence. Each step produces a necessary piece of data for the next: skipping a step or treating it in esteem results in a budget built on a fragile foundation. The sequence takes place before the kick-off, based on the estimate and the specifications.

Step 1: Frame the scope and tasks

The scope of the project is the exhaustive list of the deliverables that the company is committed to producing and the activities necessary to achieve them. The division of the project into tasks and subtasks makes the costing achievable: a fuzzy task cannot be quantified, a deliverable named yes. The framing ends with a work breakdown structure or task checklist, which serves as the basis for the next steps.

Step 2: Estimate the time per contributor (3 techniques)

Each task receives a time estimate in man-days, per contributor profile. Three estimation techniques coexist in a service company and can be combined depending on the project:

- Analogue estimation. The time is estimated by analogy with a comparable past project. Quick method, depending on the quality of the history. Suitable for recurring projects: site redesign, tooled migration, standard scoping mission.

- Parametric estimation. The time is calculated from a parameterized formula: number of screens × 1.5 days, number of users × 0.3 days of training, number of environments × 2 days of configuration. Suitable for industrialized projects where parameters are measurable.

- Bottom-up estimation. Time is calculated task by task by interviewing each contributor. The most rigorous, the longest, the most precise method. Suitable for non-standard projects and projects with high margin stakes.

A good practice is to estimate the envelope for the first time in analog, then refine it in a bottom-up way on the heaviest cost items.

Step 3: Quantify subcontracting and purchasing

For each need for external expertise, the costing of subcontracting requires three elements:

- The unit price negotiated with the subcontractor (ADR or lump sum depending on the service);

- The estimated volume in man-days or deliverables;

- The resale margin applied by the company.

For product purchases (licenses, hardware, hardware), the costing requires the purchase cost, the resale margin, and the delivery times.

These two items often account for 15 to 30% of the project budget in a service company. Subcontracting estimated without a firm quote becomes the first margin trap.

Step 4: Estimate the chargeable charges

The costs that can be rebilled to the client (travel, accommodation, catering) are calculated by estimating the missions over the duration of the project:

- Number of planned trips × average cost per trip (transportation + accommodation + meals);

- Method of re-invoicing: actual on receipts or flat rate per day of assignment;

- Repayment deadline vs. corporate cash (impact cash).

Non-rebillable costs (internal tools, pre-sales, onboarding consultant) remain estimated separately because they do not generate turnover.

Step 5: Valuation of turnover according to the contractual method

The projected turnover is calculated differently depending on the contractual method signed with the customer:

- Package. The turnover is fixed in the estimate: a total amount negotiated, paid according to an agreed schedule (deposit, intermediate deliveries, balance). The budget projects the turnover month by month according to this schedule.

- Stage management. The turnover is equal to the number of days planned× ADR invoiced. If the contract has a ceiling, the budget projects the turnover up to the ceiling. The project manager must anticipate consumption to avoid reaching the ceiling before the end of the project.

- Mixed mode. The budget separates a fixed rate board and a management board. The margin is calculated per block to remain arbitrable.

The re-invoicing of fees and product purchases is added to the main turnover, with its own resale margin.

Step 6: Calculate the target margin and the hazard

With the projected turnover and the total estimated cost established, the target margin is calculated in two stages:

- Gross margin = projected revenue − projected direct cost (man-days) ADR cost + subcontracting + non-rebillable costs).

- Net margin = gross margin − allocated overheads (management, support functions, sales cost).

On this basis, the hazard is calculated according to the method used by practice (flat-rate percentage, per position, or based on identified risks, see the section on components above).

The torque (target margin, hazard) must be validated by the practice director before the quote is signed. A project with a gross margin below the threshold of the practice goes back to commercial arbitration.

Step 7: Build the project income statement

The projected project budget takes the form of a simplified income statement, with four distinct blocks:

| Turnover | Flat-rate turnover + management turnover + re-invoicing of expenses + re-invoicing of purchases |

| Direct costs | Internal man-days (ADR cost) + subcontracting + non-rebillable costs + material + product purchases |

| Gross margin | Revenue - direct costs |

| Hazard and net margin | Provisioned contingency + residual net margin |

This structure is used to:

- Consolidate the provisional budget at practice and company level (the blocks are additives between projects);

- Compare each line with the realized during the execution;

- Justify the target margin to the sales department and the CFO.

The project income statement is the operational artefact of the provisional budget. All the other forms (flat Excel matrix, visual dashboard) derive from it.

Which tool to write a project budget?

Three families of tools coexist in a service company to write a project budget.

- Spreadsheet (Excel, Google Sheets). Maximum flexibility, zero learning curve, zero cost. Limitations: no automatic consolidation between projects, no connection with time reporting or invoicing, no projected margin calculation during execution. The spreadsheet remains valid for a small volume of simple projects (less than 10 simultaneous projects in a pure package).

- PPM or project portfolio management software. Multi-project consolidated view, dependency management, scenario simulation resource planning. Limitations: not very suitable for IT Services and consulting firms that need to integrate customer invoicing and project margin monitoring, not just the resource planning.

- ERP services or native tool service company. Connects the project budget forecast to the workload plan, time declaration, invoicing and accounting. Calculates the projected margin on an ongoing basis (see next section). This is the right family of tools for IT Services, consulting firms and agencies with 30 or more employees.

The choice is made on the basis of the couple [volume of projects] × [complexity of the contractual mode] × [expected level of margin management].

Discover project management with Stafiz

Format the budget and have it validated

The provisional project budget is used to arbitrate the signature and to steer the execution. Its formatting must therefore be readable by three distinct audiences:

- The project manager wants to see the man-days per task, the subcontractors hired, the gross margin.

- The practice manager wants to see the consolidated net margin per month and the deviation from the target margin standard.

- The CFO or management controller wants to see consolidation by customer account and by financial year, with the cash impact.

The budget is validated at three levels:

- Project manager validation : scope, man-days, subcontracting, expenses.

- Practice Director Validation : ADR, target margin, resource planning.

- CFO or management controller validation : cash flow coherence, overall workload plan, level of contingency.

On a strategic project, the sales department enters the loop to set the sale price before signing the customer.

What are the pitfalls to avoid when calculating the project budget?

Six pitfalls explain most of the budget drifts in service companies. All of them are identifiable and correctable at the time of the construction of the provisional budget, not afterwards. The common rule: do not sign the estimate until at least an explicit response has been given to each of these six points. A poor budgeting process remains one of the documented causes leading to project failure.

Pitfall 1: Underestimated costs

The most common pitfall remains the overall underestimation of man-days. The usual cause: an initial analogue estimate on a project considered comparable, never refined in a bottom-up way on heavy substations. As a result, the initial gross margin does not hold up from the first quarter of execution.

The fix involves a systematic double estimate for items representing more than 20% of the budget: an analog estimate to frame it, then a bottom-up estimate by the contributors concerned. The difference between the two estimates gives the measure of the estimation risk.

Trap 2: Bad ADR Cost

The ADR cost is not the annual salary divided by 220 days. It includes:

- The salary charged (social security contributions, mutual insurance, provident insurance);

- The bonuses provided for in the remuneration;

- The advantages (meal vouchers, transport, mobile);

- The share of indirect costs allocated by profile (premises, tools, supervision, training).

A practice that calculates its ADR costing, forgetting the indirect cost allocated, underestimates its internal costs by 15 to 25%. The apparent target margin is high at the time of the quote, but the actual margin at closing is consistently lower.

The ADR is recalculated each financial year, after the closing of the practice's accounts.

Trap 3: Uncosted subcontracting

A subcontracting estimated without a firm quote from the subcontractor transfers the margin risk to the company. The subcontractor may charge more than the initial estimate, without any possibility of recourse if the order has not been framed.

The correction: no provisional budget is signed without a firm quote from the identified subcontractors, or without an explicit provision covering the estimate/negotiation difference.

Trap 4: Absent or undersized hazard

A non-contingency provisional budget transfers the risk to the target margin: any unforeseen event increases the margin, not the provision. On a project of more than 6 months, this scheme results in a margin at completion that is regularly lower than the target margin signed.

An undersized hazard produces the same effect but more discreetly. A 3% provision on a project with high technical uncertainty (integration on a poorly documented customer system, junior team, poorly mastered technology) does not absorb anything.

The calibration of the hazard must reflect the actual risk, not a historical lump sum percentage applied by habit.

Pitfall 5: Lack of budget flexibility

An overly rigid provisional budget prevents the arbitrations of project courses. If each line is locked to the nearest euro, any reallocation of days between two profiles or any transfer between a subcontracted position and an internal position requires a complete overhaul.

The correction: set the provisional budget by envelopes (CA block, direct costs block, contingency block, margin block) by authorizing internal arbitrations for each envelope without triggering a contractual revision.

Pitfall 6: Misallocation of resources

Assigning a senior profile to a junior task increases the cost without changing the value delivered. Assigning a junior profile to a senior task degrades quality, lengthens the deadline, and often calls for a senior intervention to catch up. Both cases degrade the margin.

The fix involves a skills map × level × ADR cost kept up to date on the driving practice side, and a validation point resource planning before signing which confronts the plan of resource planning available skills. A project that does not find its way resource planning Optimal at the time of the budget signs its margin risk.

From the provisional budget to the real-time forecast margin

A specific provisional budget is only useful if you are confronted with the reality of the project in progress. In Excel, this comparison is manual and quarterly. In a dedicated tool, it is continuous. It is the gap that separates a budget that drives the margin from a budget that documents it after the fact.

Excel's limit for tracking margin during the project

On a spreadsheet, the discrepancy between the initial budget and the actual situation remains a calculation to be done by hand until the project is completed: add up the time declared to date, the subcontracting purchases and the costs incurred, then subtract everything from the recognized turnover. The result gives a margin to date, not a forecast margin.

The gap matters. A margin to date says what has happened since the kick-off. A projected margin says what the margin will be at the end of the project, including the remaining amount to be done. It is this second piece of data that is used to arbitrate a customer amendment, to reallocate resources, or to warn the CFO of a drift before it is recorded as a loss.

On a spreadsheet, the calculation of the projected margin involves:

- recover the declared time and value it at the actual cost of each employee;

- estimate the remaining work to be done per task in man-days and value it;

- Add up the costs incurred and the subcontracting invoiced.

- compared to the turnover recognised over the same period.

Each of these blocks lives in a different system: time declaration in an HR or business tool, purchases in accounting, task monitoring in a project tool, invoicing in the ERP. The consolidation work is manual, therefore rare, and therefore read too late.

The mechanism: consumed + remaining to be done = margin landing

The budget landing of a project is the projection of the final result from the data already made and the remaining forecasts. On a service project, he calculates the expected margin at the end of the project by comparing the days consumed with the initial production plan, and integrating the remaining work estimated by the project manager.

The basic formula:

Margin at completion = total projected turnover − (cost consumed to date + cost of the remainder to be made)

The cost consumed to date includes the days declared multiplied by the hourly or daily cost of each profile, the subcontracting purchases invoiced, the costs incurred. The cost of the rest to be done depends on the scope still open: tasks not started, man-days planned to complete them, subcontracting contracted but not invoiced, costs to come.

On a 100-man-day fixed-price project sold for €100k, 40 days consumed at the halfway point and a forecast of the remaining work to be done that increases to 70 days cause the margin to plunge at completion without any quarter having been closed. This is the signal that a provisional budget without monitoring the projected margin allows to pass.

The complete calculation method is detailed in the article on the budget landing in project management.

Continuous monitoring in a dedicated tool

A project management tool for a service company connects the four flows (time, purchases, expenses, invoicing) on the same project sheet and recalculates the margin at completion with each entry. The project manager sees a forecast margin that changes every week. The DAF receives an alert as soon as a drift threshold is crossed.

Budget monitoring of projects, in anticipation

See Stafiz in action in 2 minutes

It is this data, the real-time forecast margin, that separates a useful forecast budget from a decorative forecast budget.

How to rebudget during the project without breaking the customer relationship

A provisional budget is not supposed to change once validated. In reality, on a long-term project IT Services or in a consulting firm, three situations require a review: the scope changes at the client's request, the projected margin drifts without cause scope, or an internal investment decision shifts the target. The risk in all cases is the same: to let the initial budget prevail when it no longer represents reality.

Three triggers that require a re-budget

Change of scope on the customer side. The customer requests additional functionality, extends the schedule, or changes the delivery target. The new scope implies the obsolescence of the initial budget: a rebudgeted budget becomes the new reference.

Drift margin without cause perimeter. The scope has not changed but the forecast margin is plunging: initial underestimation of a task, too senior internal profile assigned to a junior task, subcontracting more expensive than expected. The initial budget remains theoretically valid but no longer says anything useful.

Internal reinvestment decision. The company chooses to commit additional man-days to a strategic project, or to redirect the turnover of a project towards the consolidation of a key account. The budget becomes an object of steering, not a fixed contract.

Draw up a costed amendment before reviewing the budget

When the cause is a change in customer scope, the budget is revised through an amendment. The amendment quantifies the additional man-days, the additional subcontracting, the new costs, and redefines the target margin. It becomes a contractual document and serves as the basis for the new budget.

Three sensitive points:

- Contractual mode maintained. A project sold on a fixed price basis remains on a fixed price basis on the amendment, unless explicitly switched to a direct contract. Mixing the two in the same amendment creates discrepancies that are difficult to arbitrate afterwards.

- Recalibrated target margin. An amendment does not automatically take over the initial margin of the project. If the additional task is more complex or if the subcontracting is more expensive, the target margin of the amendment may differ from that of the original contract.

- Documented customer communication. The amendment shall provide a justification for the new scope and its costing. This trace avoids renegotiation on delivery.

Breakpoint and arbitrage tasks when margin drifts

When the cause is an internal drift without a change in scope, the amendment is not the tool. There are three levers on the service company side:

- Reallocation of resources. Replace an over-senior profile with a profile better calibrated to the remaining tasks, or transfer a task between two consultants to reduce the hourly cost.

- Renegotiation with the client. On a project lasting several months, renegotiation remains possible if the client has an interest in seeing the project completed. It is prepared with a budgeted budget in hand, not a vague degraded margin.

- Breakpoint and task arbitration. Pause the non-essential tasks of the initial scope, the time to stabilize the others. This decision is taken by the project committee, with the quantification of the consequences.

The full method of running tracking is detailed in the article on budget tracking a project.

Examples of project budget estimates in IT Services or consulting firm

Three concrete cases of a project budget forecast in a service company illustrate the components and method presented above. The first two correspond to projects built in Stafiz and set out the typical format of a projected project budget. The third presents a 6-month IT project where the monitoring of the projected margin has prevented a drift during execution.

Example 1: Simple flat rate project, human intervention

For a project sold on a fixed-price basis with only human intervention (redesign of an internal application, standard scoping mission, organizational audit), the provisional budget remains compact. Five lines are enough:

- Internal man-days by profile× ADR cost;

- Rebillable fees;

- Target gross margin;

- Hazard;

- Turnover fixed in the quote.

Project costing in Stafiz

This format is suitable for 70% of consulting firm projects and for the majority of short projects in IT Services.

Example 2: Mixed project with subcontracting and licensing

For a more complex project combining internal contributors, subcontractors, license purchases and travel expenses (IT integration project, transformation mission, multi-site deployment), the provisional budget extends:

- Internal man-days by profile× ADR cost;

- Subcontracting by service provider (purchase price + resale margin);

- Product purchases (licenses, hardware);

- Rebillable expenses (travel, accommodation);

- Target gross margin per block;

- Hazard by position;

- Flat rate turnover + rebilling fees + resale products.

Project costing with license sales and subcontracting

This format is suitable for integration projects in IT Services, consulting firm transformation projects and multi-site projects.

Example 3: 6-month IT project with controlled drift

On a 6-month software integration project sold for €240k at a fixed price to an ETI client, the provisional budget was built with:

- An internal cost of €175k (75 senior man-days + 90 intermediate man-days + 30 junior man-days);

- A subcontracting of 25 k€ (20 man-days freelance application security);

- Flat-rate rebillable fees of €8k;

- A €12k hazard;

- A net target margin of €20k.

At the halfway point, the internal man-day consumption showed 95 man-days consumed out of the 195 planned (49%), in compliance. But the forecast of the remaining work was increased to 135 man-days instead of the 100 initially planned. The projected margin at completion plunged from €20k to −€8k.

Three actions were triggered in the month following the detection:

- Reassignment : an integration task assigned to a senior has been switched to an intermediate profile (estimated savings of €12k);

- Negotiated amendment : an additional deliverable requested during the project was costed at €18k, which moved the turnover to €258k;

- Stopping point : two non-essential tasks of the initial scope have been postponed to post-delivery (savings 9 k€).

At closing, the final net margin was €17k, compared to the €20k target at the outset. Without the monitoring of the projected margin during execution, the deviation would have been detected at the quarter close, too late for the three arbitrage levers.

Building a provisional budget for projects line by line is the step taken. Comparing it in real time with the provisional margin at completion is the next step, and it is this step that separates a budget that drives the margin from a budget that documents it after the fact.

To test the construction of a project budget and the monitoring of the projected margin in Stafiz, do not hesitate to contact us!

Frequently asked questions:

On a project in a service company, three types of budget coexist: the provisional budget (estimate made before the kick-off, sets the target margin), the committed budget (part of the forecast contracted by orders and schedules), and the realized budget (cost and turnover actually recorded to date). A fourth budget exists for long projects: the landed budget, which projects the final result by combining what has been achieved and what remains to be done.

The drafting of a project budget follows three main phases: (1) identify resource needs (man-days per profile, subcontracting, purchasing, costs); (2) estimate the costs for each item from the ADR cost and negotiated prices; (3) structure the budget in the form of a project income statement, including the target margin and the risk provision hazard.

The budget is a numerical target for a period of activity (month, quarter, financial year) at the company or practice level. The provisional budget is an estimate projected before implementation, placed at the project or activity level. On a service project, the projected project budget is the operational unit: it is set before the kick-off and serves as a reference throughout the duration of the project. Several project budgets are consolidated into a practical annual budget.

The provisional budget is the estimate made before implementation. The actual budget is the record of what has actually been spent and invoiced once the period has passed. On a project in progress, these two notions are not enough: the margin at completion combines what has been achieved to date and the cost of the remainder to be done to project the final result. It is this third data that is used to arbitrate during execution.

A provisional project budget in IT Services or consulting firm covers eight components: (1) internal contributors valued at the ADR cost; (2) subcontracting with resale margin; (3) products and purchases (licenses, hardware); (4) Used hardware and its depreciation; (5) rebillable and non-rebillable expenses; (6) turnover according to the contractual mode (fixed-rate, time-owned, mixed); (7) target margin (gross and net); (8) contingencies and provision of risks. The final format takes the form of a project income statement in four blocks.

On a project in a service company, three roles participate in the construction of the provisional budget: the project manager calculates the scope, estimates the man-days and identifies the needs for subcontracting; The Practice ( or Mission) Director validates the ADR, target margin levels and profile arbitrages; the project management controller or CFO checks the consistency with the company's budget assumptions and the projected workload plan. On a strategic project, the sales department enters the loop to set the selling price.

The provisional project budget is built before the contract is signed, based on the estimate and the specifications. It serves as a reference throughout the duration of the project. It is revised in three cases: a change in the client's scope validated by an amendment, a margin drift without cause in the scope, or an internal decision to reinvest. On a recurring project or a key account, the budget can also be revised at the beginning of each year by integrating known commitments.

The calculation of a projected project budget is based on two complementary formulas: Estimated total cost = (internal man-days× ADR cost) + subcontracting + purchases + material + non-rebillable costs. Projected gross margin = projected turnover − total estimated cost. The hazard is then added to the target margin in the form of a provision: a lump sum percentage, per item, or based on identified risks. During execution, the margin at completion is calculated by replacing the total estimated cost with: cost consumed to date + cost of the remaining costs.

A project budget table is filled in according to the seven steps of the method presented above (framing the scope, estimating the time per contributor, quantifying subcontracting, estimating costs, valuing turnover, calculating margin and contingency, building the income statement). A downloadable Excel template is available on the dedicated page: project budget table.