Project management With Financial and Operational Constraints

Delivering value to clients while keeping costs in check requires a delicate balance inprofessional services.The only way to maintain this balance is through efficient resource utilization, maintaining high service quality, monitoring project metrics, identifying potential risks, developing effective risk mitigation strategies, and ensuring compliance with standards.

Project management often unfolds within the context of stringent financial and operational constraints. Most professional service providers are constantly confronted with challenges, including delivering value for clients while keeping costs competitive.

Many projects are undertaken on a fixed-price basis, which means that any cost overruns come out of the provider's pocket. It's essential to carefully manage costs to protect profit margins. Resource efficiency is essential to keeping costs in check and requires optimized project management and scheduling to minimize non-billable hours.

Similarly, for time and materials projects, professional services need to monitor project billing to ensure they are paid on time.

Professional services firms must also implement a robust risk management process to identify and mitigate potential risks. This involves assessing potential risks, developing contingency plans, and implementing risk mitigation strategies. A thorough understanding of the project and industry-specific regulations is essential for developing effective risk mitigation strategies.

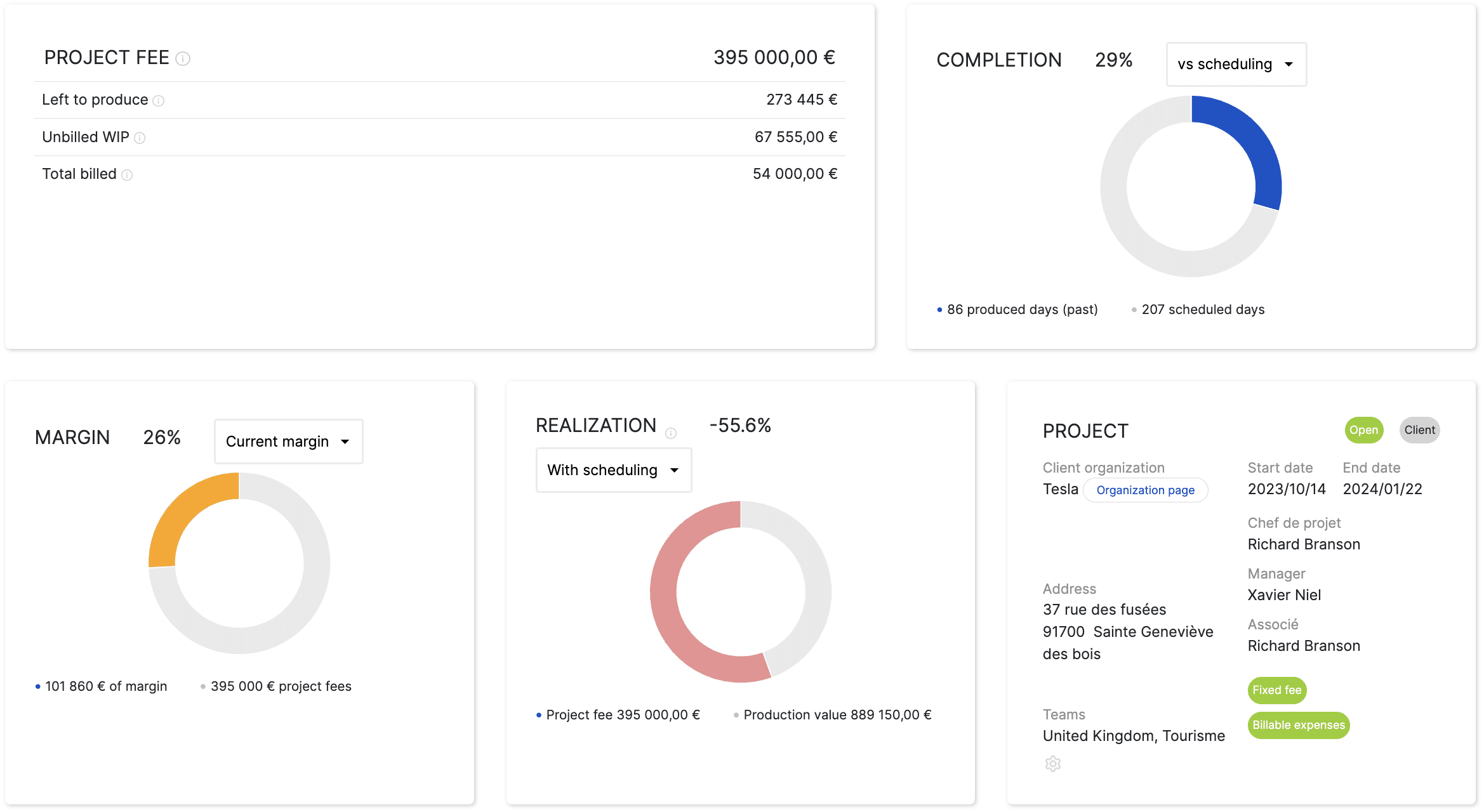

Project metrics can help professional services firms to track their progress and risks and ensure that they are delivering value to clients on time and within budget. Investing in tools that will automate data collection, analysis and reporting processes can reduce human error, simplify the entire process and gain time.

Project Portfolio Management

Project portfolio management (PPM)takes a holistic approach that helps organizations align their projects with overarching business strategies and objectives. PPM ensures that resources, time, and investments are allocated to initiatives that will have the most significant impact on an organization's growth and success.

This strategic alignment ensures that resources, both human and financial, are directed toward projects that directly contribute to the organization's long-term goals, which helps companies avoid wasting valuable resources on initiatives that don’t align with their strategic direction. Projects that are strategically aligned tend to yield a higher return on investment. By investing in projects that support the organization's core objectives, the likelihood of achieving meaningful ROI is significantly increased.

When projects are in sync with business strategies, it becomes easier to identify potential risks and align mitigation strategies accordingly. This proactive approach minimizes potential disruptions and setbacks. Aligning projects with business strategies also empowers organizations to make informed decisions about which projects to prioritize, expand, or terminate. It also fosters better collaboration and communication among teams.

There are several key steps in effective Project Portfolio Management (DPM):

Step 1: Define the organization's goals and objectives.

The first step in PPM is to define the organization's goals and objectives. This will help to ensure that all projects are aligned with the organization's overall goals and objectives. The objectives should be specific, measurable, achievable, relevant, and time-bound.

Step 2: Identify and evaluate potential projects.

Once the organization's goals and objectives have been defined, the next step is to identify and evaluate potential projects. This involves brainstorming a list of potential projects and then evaluating each project based on its potential benefits, risks, and resource requirements. The evaluation process should help to identify the most promising projects for the portfolio.

Step 3: Select projects for the portfolio.

Once the potential projects have been evaluated, the next step is to select projects for the portfolio. This is done by considering the organization's goals and objectives, the available resources, and the potential risks and benefits of each project. The organization should also consider its risk tolerance when selecting projects for the portfolio.

Step 4: Prioritize the projects in the portfolio.

Once the projects have been selected for the portfolio, the next step is to prioritize them. This is done by considering the importance of each project to the organization, the urgency of the project, and the project's dependencies. The organization should prioritize the projects that are most important to its goals and objectives, and that have the highest potential benefits.

Step 5: Plan and execute the projects.

Once the projects have been prioritized, the next step is to plan and execute them. This involves developing detailed project plans, assigning resources, and tracking progress. The project plans should be realistic and achievable, and they should be aligned with the organization's goals and objectives.

Step 6: Monitor and control the portfolio.

The final step in PPM is to monitor and control the portfolio. This involves regularly reviewing the portfolio to ensure that it is aligned with the organization's goals and objectives, and to make adjustments as needed. The organization should also monitor the project performance to ensure that it is on track and meeting its goals.

Effective leadership and communication

The ability to lead and communicate effectively is a defining factor for success in professional services project management. It is not only about managing timelines, resources, and deliverables; it is also about fostering a collaborative environment and breaking down silos within an organization.

Project governance, distinct from project management, is a global methodology focused on strategic objectives. It involves defining procedures and allocating resources, serving as a vital method for business sustainability. Project governance requires alignment with the overall company strategy and demands strategic decision-making by management teams. The implementation of project governance addresses challenges like aligning projects with strategy, facilitating decision-making, optimizing resource management, ensuring sustainability, and improving communication by breaking down silos.

Silos refer to the division of departments or teams, often resulting in poor cross-functional communication and collaboration. Leaders can break down silos by:

- Implementing clear and open communication channels that encourage teams from different departments to collaborate.

- Fostering a culture of information sharing and knowledge transfer.

- Forming cross-functional project teams that bring together members from different departments to work on a project to promote understanding.

- Investing in project management tools that offer a unified platform for all project-related data and communication, ensuring that everyone involved has access to the same information and can collaborate effectively.

- Breaking down their own silos by actively collaborating with other departments and fostering a culture of teamwork and open communication.

- Holding regular cross-departmental meetings and status updates to keep everyone informed about the project's progress. These meetings also provide an opportunity for stakeholders to share insights and concerns.

With the right leadership and communication strategies, coupled with the aid of modern automation tools, project managers can navigate the complex landscape of project management, foster collaboration, and drive their projects towards successful outcomes.

Managing Client Expectations and Scope

Balancing client demands with project feasibility is a challenge that professional service providers face daily. Scope creep is a common and persistent challenge that professional service providers grapple with in their day-to-day operations.

Clients may not have a full understanding of the project's intricacies, leading to evolving expectations as the project unfolds. These evolving expectations can push the project beyond its initial scope. Poor communication between the client and the service provider can also result in misunderstandings, leading to scope changes.

Scope creep is a common challenge inprofessional services, but it can be avoided. Clearly define the project scope at the outset by outlining the project's objectives, deliverables, constraints, and assumptions. Frequent communication helps to ensure that the client is aware of the project's progress and any potential changes to the scope. It is important to keep the client informed of any changes to the scope and to get their approval before proceeding. Project management tools and techniques can help to track progress, manage resources, and identify potential risks. This can help to keep the project on track and prevent scope creep.

How an ERP for professional software services can help

Managing client expectations and resources, managing projects under financial constraints, and implementing project portfolio management best practices while breaking down silos can be a challenge. Even a dedicated project manager and leader cannot do this without the assistance of best-of-breed project management automation technology.

If you'd like to learn more, request a demo. We'd love to help you transform project management within your professional services firm or entity.